At 2.15 Banksters Bail In Law: Legal For Banks to Steal Your Deposited Money; Glass-Steagall Needed to Protect Depositors From Swindle

Economic Collapse News February 23, 2020.

Things are heating up in as citizens surround a Bank in Yichun, Jiangxi China. This brings us to an important point, cash is king. Now it’s clear the Central banks are going to print until they run out of paper and the Dollar will inevitably lose value but in the meantime having cash set aside for times of distress is always a good idea. Especially if there is an instance where large banks begin to fail. The bail in-laws have never been used in the US but if a systemically important financial institution fails due to economic collapse we may see just that. So it’s good to have access to your money. In Italy, we see there is a significant amount of people who have been asked to remain inside and several thousand in the US unless all of these people work online they will eventually run out of money.

INTRODUCTION

The 1999 repeal of the original “Glass-Steagall Act” of 1933 was perhaps the single greatest criminal act committed against the economic welfare of the American people in the 20th Century. Despite all claims to the contrary, the repeal of Glass-Steagall laid the groundwork for the creation of a monstrous derivatives bubble which burst during the financial crisis of 2007-2008. Following that crash, the first act of Congress should have been to correct their folly by restoring Glass-Steagall, thus eliminating the massive bubble of gambling values and erecting a firewall between the uncontrolled speculation on Wall Street and the livelihood of the American people — precisely as Franklin Roosevelt did in 1933 when the Glass-Steagall Act was first enshrined into law. Instead, under the threats and intimidation of the largest financial institutions, Congress passed an unprecedented bailout of the Wall Street banks, on the backs of an already destitute American population. Over the subsequent eight years, our people have suffered the mounting effects of this fraud, to the point that our nation now faces another financial blowout of far-greater magnitude than even that of 2007-2008. The only means of avoiding such a fate is the immediate restoration of Glass-Steagall today as the necessary first step to a full FDR-style recovery program, as has been spelled out in detail by LaRouchePAC.

Glass-Steagall put properly, is not a federal regulation aimed at restraining the criminal temptations of an otherwise happy-go-lucky Wall Street. Glass-Steagall’s aim is to “throw the money changers out of the temple of our civilization”, once again, as President Franklin D. Roosevelt had the courage to do. It is not an adjustment within an otherwise operable system. Glass-Steagall is a revolution in national policy, a Declaration of Independence against an oppressive regime.

Glass-Steagall will not regulate Wall Street, but destroy it, and put it out of its misery, once and for all. America does not need Wall Street for its economy to grow any more than a tumor would be helpful to the growth of a man. The American Credit System, long advocated by Lyndon LaRouche, is the historical beacon with which finance the nation’s future. The cult of Wall Street—the system of finance characterized by increased rates of gambling, stealing, and fraud, has, once again, nearly destroyed the United States and therefore itself. Like a cancer, it must kill you in order for it to stay alive.What’s At Stake?Just How Bad Is It?The Triple CurveTotal DerivativesHow Did It Get This Bad?Takedown of Glass-SteagallNomi Prins on Glass-Steagall“Nobody Could Have Known”LaRouche on the Record 2008“But, Give Dodd-Frank a Chance!”The Fight For Glass-Steagall TodayContact your member of CongressNational and International SupportS.881H.R. 790

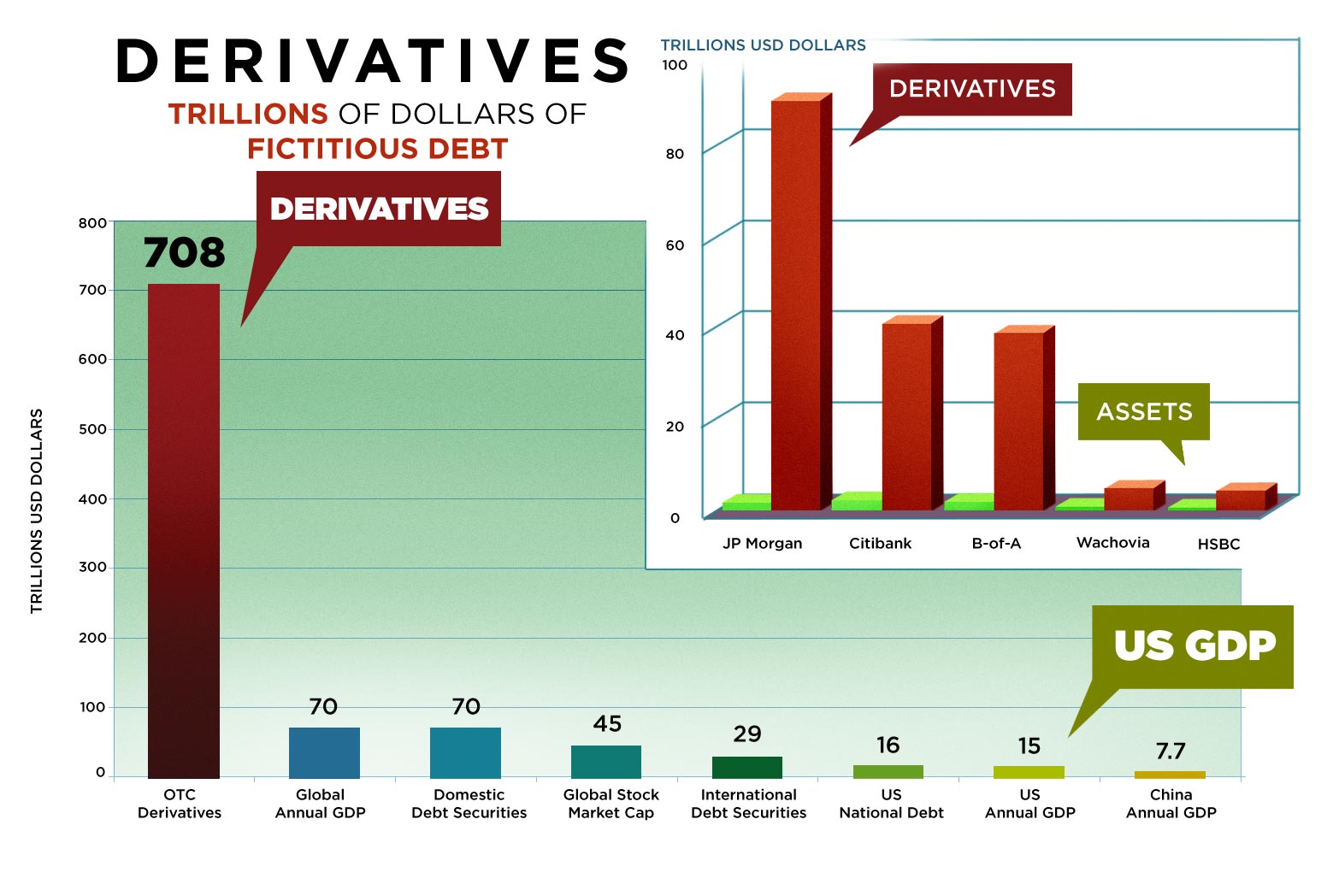

Estimates are that the current magnitude of outstanding derivatives claims accumulated as a product of speculative financial practices (read: gambling debts), now measures in the hundreds of trillions of dollars, perhaps reaching even to quadrillions. Even when compared to the current nominal global GDP, estimated at around $70 trillion, it becomes immediately apparent that this debt can never be paid. The vast majority of these outstanding claims are of a purely speculative character, with absolutely no connection to legitimate, necessary, productive economic activity. To continue to bail out this vast bubble of gambling obligations on the back of a collapsed and rapidly shrinking real economy, would be to create, rapidly, Weimar-style hyperinflation on a global scale, and an economic crisis of Dark Age proportions.

“The Triple Curve” was first presented by Mr. LaRouche at a conference at the Vatican in 1995. The version seen above is the third in a series, and functions as a heuristic device to describe the generalized collapse function of the world economy since 1971. The only way to stem the further collapse of the system is by using a Glass-Steagall standard to reorganize the transatlantic economy such that the monetary and financial aggregates of the economy conform to an increase in the physical economic input-output of the system, versus a decrease.

Glass-Steagall halts this catastrophe. By restoring the separation between commercial and investment banking, Glass-Steagall divides the obligations in question into two distinct and separate categories: legitimate and illegitimate, the latter being far greater than the former. Immediately, we declare that the government has no responsibility to pay back losses accrued through speculative activity, thus transferring these trillions in liabilities off of the government’s books. We force the megabanks—JP Morgan Chase, Citigroup, Morgan Stanley, etc.—to split themselves in two parts: the so-called “investment arms” on the one side, and plain, old-fashioned commercial banking on the other.

Under the original Glass-Steagall law, only commercial banks receive federal guarantees; “investment houses” do not enjoy such protection. Though their trillions in outstanding “assets” might not be explicitly cancelled or eliminated by law, we will simply declare that these debts are their own, their responsibility, and not the American people’s. Not one penny of bailout goes to pay them off, and, without this artificial protection, these assets will quickly dry up on their own. We as a nation are freed from this cancer, and our commercial banking system is restored to its necessary and indispensable function. This was the stated intention of Franklin Roosevelt’s original 1933 Glass-Steagall Act.

How Did It Get This Bad?

Originally produced in September 2010, LaRouchePAC’s “The Takedown of Glass-Steagall” provides the historical context for the crisis we are in today. This was LaRouchePAC’s challenge to the Democratic Party: to survive, it must cease being the party of Barack Obama and the Wall Street interests who own him. These historic oligarchic interests are what is destroying the United States today, by controlling key elected officials, such as then chairman of the House Financial Services Committee, Barney Frank, author of Obama’s infamous Wall Street reform legislation. The American people must go over the heads of Congress and the President, cut a wedge through party lines, and deliver themselves the prosperity they require.

Nomi Prins on Glass-Steagall

Nomi Prins delivers remarks to the Schiller Institute’s 30th anniversary conference, discussing her latest book “All The Presidents’ Bankers,” which details the “historical alignment of the White House and Wall Street” from Teddy Roosevelt to Barack Obama.

In 2007, during a live, international webcast, Lyndon LaRouche made a prophetic economic forecast:“There is no possibility of a non-collapse of the present financial system—none! It’s finished, now! The present financial system can not continue to exist under any circumstances, under any Presidency, under any leadership, or any leadership of nations. Only a fundamental and sudden change in the world monetary-financial system will prevent a general, immediate chain-reaction type of collapse. At what speed we don’t know, but it will go on, and it will be unstoppable!”

Then, in 2008, LaRouche was one of the first and only economists who knew that without a Glass-Steagall reorganization of the transatlantic economy, there would be no hope for a recovery.

“Bail-in, in its simplest terms, is the inverse policy of what was done under Franklin D. Roosevelt’s Glass-Steagall Act and the 1933 Banking Act generally. Under bail-in the bank survives, the depositors do not.”“The preceding provisions of law and international agreements have been made in such a way that places the interests of “financial stability” above the interests of the people of the United States and their Government.

On a 2012 LPAC Activist call, EIR‘s Jeff Steinberg provides the broader implications of a Glass-Steagall reorganization for the global financial system and gives a blow by blow account of the battle to include Glass-Steagall in what became known as “Dodd-Frank”.