When Crypto-Exchanges Go Broke, You’ll Lose It All

When Crypto-Exchanges Go Broke, You’ll Lose It All

The fatal flaw in the ‘neither fish nor fowl’ gambit

If you’ve spent much time around cryptocurrency people, you’ve probably heard a rant or two about “sound money” and the need to “depoliticize money.” This is a foundation of blockchainism: the belief that money is born separate from states, and states invade on the private realm when they “meddle” in the money system.

There are at least two serious problems with this ideology. First, it’s plain wrong on the historical facts. Money did not emerge from barter systems among people. Money was and is a product of states:

https://www.theatlantic.com/business/archive/2016/02/barter-society-myth/471051/

But even if you stipulate that money didn’t originate among private markets (and I’m fully aware that there are many Reply Guys who will @ me to tell me that they disagree), there’s another serious historical problem with “sound money.”

It’s this: Central banks didn’t emerge to usurp the private sector’s control over money. Central banks were created because without them, finance was subject to wild, terrifying, ruinous boom/bust cycles. What’s more, without a central bank, money was subject to naked political meddling, which central banks (sometimes) moderated.

The idea that a society can survive without a state or other actor that can create and destroy money based on prevailing economic conditions is both ahistorical and impractical. If we all adopted cryptocurrency tomorrow, there’d still be an elastic money supply, as Yanis Varoufakis explains in this interview with The Crypto Syllabus:

https://the-crypto-syllabus.com/yanis-varoufakis-on-techno-feudalism/

“What would banks do? They would lend in Bitcoin, of course. This means that overdraft facilities would emerge allowing lenders to buy goods and services with Bitcoins that do not yet exist. What would governments do? At moments of stress, they would have to issue units of account linked to Bitcoin (as they did under the Gold Exchange Standard during the interwar period). All this private and public liquidity would cause a boom period before, inevitably, the crash comes. And then, with millions of people wrecked, governments and banks would have to abandon Bitcoin.”

The blockchainist’s insistence on “de-politicizing” money is a dead-end, in more ways than one. Actual money, run by actual states who charter actual banks, has rules — reporting rules, insurance rules, taxation rules.

The stated dream of the blockchain is to replace those rules with “private agreements,” but if you but scratch the surface of this dream, you find the age-old dream of the goldbug: money without taxation.

Thus it is that crypto people have long insisted that their coins and tokens are neither fish nor fowl: neither a currency subject to currency controls, nor a regulated security, nor an asset subject to capital gains. The ideal crypto asset is in a state of durable quantum indeterminacy, immune to collapse even when it is observed by a tax-collector.

This may (may!) make crypto immune to some kinds of tax and regulation, but it also means that crypto may be exempt from the protections that are afforded to people who own conventional assets.

Writing in Credit Slips, Adam Levitin examines the (lack of) bankruptcy protection for people who entrust their assets to crypto exchanges. It’s grim reading.

Almost everyone who uses crypto relies on these exchanges. In theory, it’s possible to manage all your own keys and transactions, but in practice, it’s a complex, error-prone, high-stakes business. Even if you can manage it, the people you’re hoping to transact with likely can’t, meaning that nearly everyone involved with cryptos has an account with one or more exchanges.

And the exchanges don’t have a great history. Mt. Gox, the first successful exchange, collapsed in a fraud-riddled bankruptcy. QuadrigaCX, Canada’s largest exchange, collapsed when its founder died without any succession plan for the keys needed to access the hundreds of millions he controlled:

https://newsinteractives.cbc.ca/longform/bitcoin-gerald-cotten-quadriga-cx-death

Crypto exchanges, projects and communities keep vanishing overnight as their founders are revealed to be scammers engaged in “rug pulls” or mere incompetents in over their heads. When that happens, the informal nature of these projects leaves the backers with little or no recourse.

All this is in stark contrast to the traditional finance sector — itself hardly a paragon of fairness and probity, but still far more legally responsible to depositors than, say, Coinbase.

Let’s start with that word “depositor.” Levitin makes a good case that legally, when you “deposit” a crypto-coin with an exchange, it’s a sale, not a deposit, with the “possessory interest” going to the exchange, not you.

If the exchange goes bust, a “bankruptcy estate” is created, and those coins become its property, as do any coins that have been staked (placed in escrow) via the exchange.

Thus, you are not a depositor in the exchange, you are a creditor. When trustees oversee a bankruptcy, they line up the creditors based on their liquidation preference. Secured creditors get first dibs on whatever is in the estate. Once they’ve been satisfied, the remainder is divvied up among the unsecured creditors.

In the case of a crypto exchange, the secured creditors are the funds, investors, and financial institutions that extended credit to the exchange. You and your fellow “depositors” are unsecured creditors. You are last in line to gain access to the bankruptcy estate’s assets. If those assets run out before it’s your turn, you get nothing.

But let’s say you were entitled to something when the bankruptcy was finalized — your assets are frozen until that finalization takes place. And if the crypto exchange just happens to be doing a lot of deliberately opaque, complex stuff to dodge taxes and regulation, you might have a very long wait.

How long? Well, Lehman Brothers incorporated over 6,000 subsidiaries and sister companies in over 100 countries in order to duck taxes, oversight and regulation. When it collapsed, it took more than five years for the bankruptcy trustees to unwind all this complexity. For half a decade, all those funds were frozen.

And even if you do get paid, you’ll be paid at the dollar value of your assets on the eve of the collapse. If your coins double in value over the years it might take to unwind a complex bankruptcy, your prorated share will be based on their value when the exchange tanked.

It gets worse. If an exchange declares bankruptcy, it can legally claw back many of the withdrawals its depositors made over the 90 days before the bankruptcy. So if you think Coinbase is looking shaky and take your money out, you’d better hope they last for at least three more months, or you might have to give the money back to the bankruptcy trustees.

Not every bankruptcy locks up every asset. There are exemptions for assets related to conventional securities contracts, swaps, repos, and forward contracts that let their owners get them back before the bankruptcy is settled. But none of that applies to exchanges.

Likewise, clawbacks might be prevented if cryptos were definitely regulated securities. Making that happen would involve a bunch of former exchange customers going to court to argue that these were regulated securities all along. You can bet that if they do that, everyone who hasn’t lost their crypto will go to court to argue the reverse, because otherwise, they lose all their regulatory and tax advantages and might have to pay whacking great sums.

Keep in mind, all of this is a feature of cryptos, not a bug. The point of the “sound money” delusion is to take money out of the realm of democratic state control and move it into a wild west of caveat emptor and smart contracts.

The current protections for bank depositors were established after ghastly crises that destroyed lives. The goldbug/cryptobug’s insistence on ignoring that history means that they are doomed to repeat it — and take all the naïve people who buy into their “investment” schemes with them.

Cory Doctorow (craphound.com) is a science fiction author, activist, and blogger. He has a podcast, a newsletter, a Twitter feed, a Mastodon feed, and a Tumblr feed. He was born in Canada, became a British citizen, and now lives in Burbank, California. His latest nonfiction book is How to Destroy Surveillance Capitalism. His latest novel for adults is Attack Surface. His latest short story collection is Radicalized. His latest picture book is Poesy the Monster Slayer. His latest YA novel is Pirate Cinema. His latest graphic novel is In Real Life. His forthcoming books include Chokepoint Capitalism: How to Beat Big Tech, Tame Big Content, and Get Artists Paid (with Rebecca Giblin), a book about artistic labor market and excessive buyer power; Red Team Blues, a noir thriller about cryptocurrency, corruption and money-laundering (Tor, 2023); and The Lost Cause, a utopian post-GND novel about truth and reconciliation with white nationalist militias (Tor, 2023).

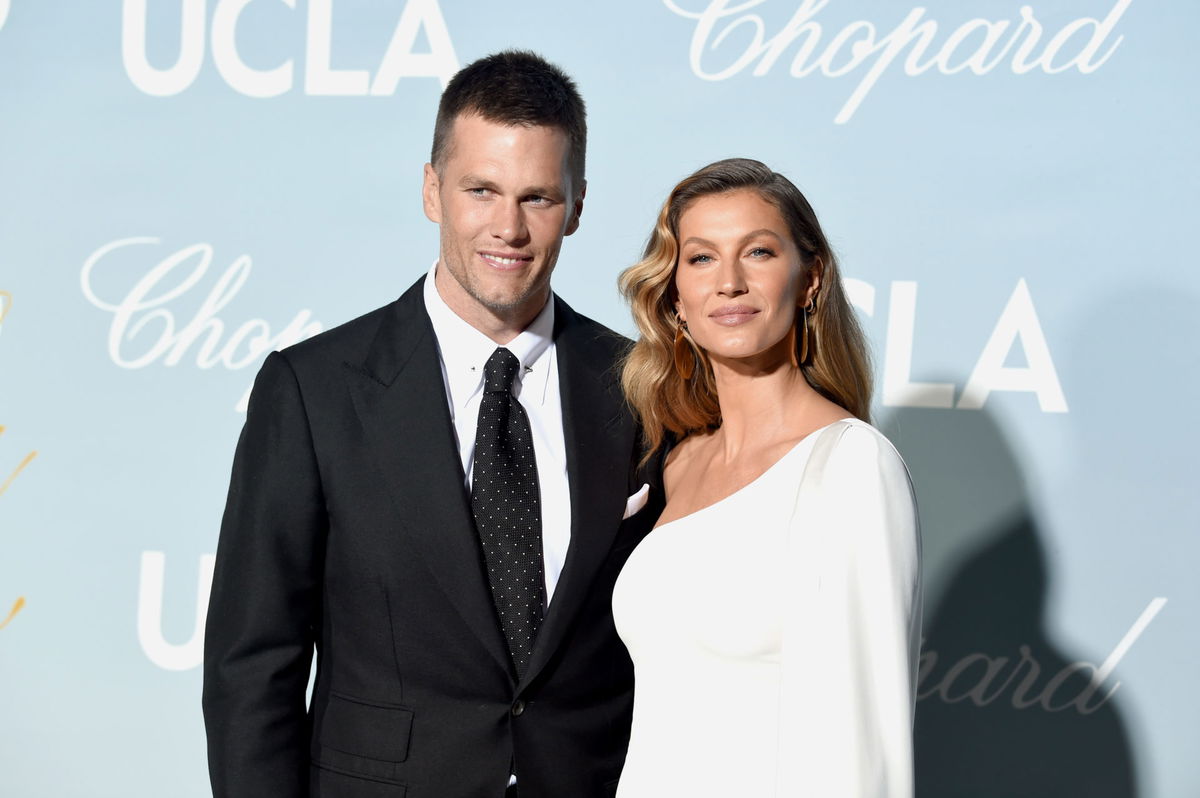

Tom Brady and Gisele Bündchen Attached A Large Sum of Their Net Worth of $600 Million Into FTX Venture That Has Now Seen a 72% Drop in Value

Comment : They have lost $432 MILLION of their net worth. The original $600 Million is now $168 million. Plus they are being sued by other investors. Since they lost so much money and apparently sincerely believed in this Crypto platform I kinda wonder if the lawsuit against them will be successful. I imagine it depends on Securities Regulations and how much liability they have for promoting the FTX Venture.

It is just not getting any better for Tom Brady this year. He went through a divorce with his wife Gisele Bündchen, and his team’s on-field form has been questionable this season. Just when he led the Tampa Bay Buccaneers to a galvanizing win over the reigning Super Bowl champions, Los Angeles Rams, he had bad news waiting for him again.

A cryptocurrency exchange in which Brady and Bündchen had invested last year has seen a 72% drop in value. And Binance is now set to buy it out.

ADVERTISEMENT

Article continues below this ad

Tom Brady and Gisele Bündchen investing big into FTX

June 2021 was a good time for Tom Brady. He had just won the Super Bowl for the seventh time a few months back. And it was a good time to invest in the cryptocurrency market as well. So Brady and his now ex-wife, Gisele Bündchen, signed a deal with the cryptocurrency exchange FTX that month.

ADVERTISEMENT

Article continues below this ad

It was an equity deal that made Brady the brand ambassador of the company. The deal also gave Bündchen an environmental and social initiatives adviser role in the company. And the couple attached a lot of their $600 million net worth into the investment.

Fast forward to 2022, the exchange has dropped 72% in value. The cryptocurrency market is in shambles. And crypto giant Binance is set to buy out the company in pennies over a dollar. That may see both Brady and Bündchen lose a major chunk of their net worth. Just another bad day for the NFL G.O.A.T.

Brady’s abysmal year

2022 hasn’t been a good year for Tom Brady. In October, his wife and supermodel Gisele Bündchen finalized the divorce with the Tampa Bay Buccaneers star. They married each other in 2009.

ADVERTISEMENT

Article continues below this ad

Bündchen wanted Brady to spend more time with the family. Brady announced his retirement from the NFL after the 2021 season to do just that. But he quickly changed his mind and came back out of it in just over a month. He wanted to win another Super Bowl ring. That did not go down well with Bündchen.