These European Banks Were Bailed Out By the American Taxpayers in 2008 and Are On Verge of Collapse Now; Oh That’s Right a Bank BAIL-In is Coming!

7 May, 2022 11:23HomeBusiness News

European banks reveal cost of Russia exit

Sanctions wiped out billions from major lenders

© Getty Images / Svetlana Davis / EyeEm

The need to write down assets as well as setting aside cash to shield against the expected economic ramifications of anti-Russia sanctions has resulted in billions of euro in losses for European banks.

The lenders have so far taken a hit of about $9.6 billion, led by Societe Generale and UniCredit. ING and Intesa Sanpaolo reported that Russian exposure had slashed their combined first-quarter net income by nearly $2 billion.

Several lenders have said their outlooks for the year would be scrapped if the drag of the Russia-Ukraine conflict on the global economy worsens. Intesa has reportedly cut its 2022 profit target, warning that a “very conservative” scenario envisions an even harder blow.

Faced with this extreme uncertainty, the chief risk officers of several European banking majors are holding meetings with regulators and among themselves to assess the reliability of their models and provisioning, people familiar with the matter told Bloomberg.READ MORE: Russians may be banned from buying EU real estate

“Corporate insolvencies in our markets will probably rise” in 2022 amid surging energy prices, high inflation and supply-chain disruptions, according to Commerzbank Chief Executive Officer Manfred Knof, who was quoted by the agency.

UniCredit said it can absorb the latest macroeconomic knock-on effects in its wider business thanks to its “strong” capital levels, asset quality and prudent loan loss reserves. One of the European banks with the biggest presence in Russia, UniCredit reportedly took a $2 billion hit as it considers an exit strategy.

Meanwhile, French lender Societe Generale is expected to take a €3 billion loss from the sale of its stake in Russia’s Rosbank.

For more stories on economy & finance visit RT’s business section]

Why Bank Bail-Ins Will Be the New Bailouts

By RICHARD BEST Updated August 31, 2021Reviewed by ROBERT C. KELLY

The financial crisis of 2008 ushered in the term “too big to fail,” which regulators and politicians used to describe the rationale for rescuing some of the country’s largest financial institutions with taxpayer-funded bailouts. Heeding the public’s displeasure over the use of their tax dollars in such a way, Congress passed the Dodd-Frank Wall Street Reform and Consumer Act of January 2010, which eliminated the option of bank bailouts but opened the door for bank bail-ins.

Difference Between Bank Bail-In and Bank Bailout

A bail-in and a bailout are both designed to prevent the complete collapse of a failing bank. The difference lies primarily in who bears the financial burden of rescuing the bank. With a bailout, the government injects capital into the banks to enable them to continue to operate. In the case of the bailout that occurred during the financial crisis, the government injected $700 billion into some of the biggest financial institutions in the country, including Bank of America Corp. (NYSE: BAC), Citigroup Inc. (NYSE: C) and American International Group (NYSE: AIG). The government doesn’t have its own money, so it must use taxpayer funds in such cases. According to the U.S. Treasury Department, the banks have since repaid all of the money.

With a bank bail-in, the bank uses the money of its unsecured creditors, including depositors and bondholders, to restructure their capital so it can stay afloat. In effect, the bank is allowed to convert its debt into equity for the purpose of increasing its capital requirements. A bank can undergo a bail-in quickly through a resolution proceeding, which provides immediate relief to the bank. The obvious risk to bank depositors is the possibility of losing a portion of their deposits. However, depositors have the protection of the Federal Deposit Insurance Corporation (FDIC), insuring each bank account for up to $250,000. Banks are required to use only those deposits in excess of the $250,000 protection.

As unsecured creditors, depositors and bondholders are subordinated to derivative claims. Derivatives are the investments that banks make among each other, which are supposed to be used to hedge their portfolios. However, the 25 largest banks hold more than $247 trillion in derivatives, which poses a tremendous amount of risk to the financial system. To avoid a potential calamity, the Dodd-Frank Act gives preference to derivative claims.

Bail-Ins Become Statutory

The provision for bank bail-ins in the Dodd-Frank Act was largely mirrored after the cross-border framework and requirements set forth in Basel III International Reforms 2 for the banking system of the European Union. It creates statutory bail-ins, giving the Federal Reserve, the FDIC and the Securities and Exchange Commission (SEC) the authority to place bank holding companies and large non-bank holding companies in receivership under federal control. Since the principal objective of the provision is to protect the American taxpayers, banks that are too big to fail will no longer be bailed out by taxpayer dollars. Instead, they will be ‘bailed in.’

Europe Experiments With Bail-Ins

Bank bail-ins have been used in Cyprus, which has been experiencing high debt and possible bank failures. The bail-in policy was instituted, forcing depositors with more than 100,000 euros to write off a portion of their holdings. Although the action prevented bank failures, it has led to unease among the financial markets in Europe over the possibility that these bail-ins may become more widespread. Investors are concerned that the increased risk to bondholders will drive yields higher and discourage bank deposits. With the banking systems in many European countries distressed by low or negative interest rates, more bank bail-ins are a strong possibility.

Comment: Since Rothschilds own all the central banks in these countries they and their criminal cohorts of the British Empire will benefit!

========================================================================

The Solution: Glass-Steagall & U.S. Needs to Join the BRICs! This will be the END for the Int’l Criminals.

INTRODUCTION

The 1999 repeal of the original “Glass-Steagall Act” of 1933 was perhaps the single greatest criminal act committed against the economic welfare of the American people in the 20th Century. Despite all claims to the contrary, the repeal of Glass-Steagall laid the groundwork for the creation of a monstrous derivatives bubble which burst during the financial crisis of 2007-2008. Following that crash, the first act of Congress should have been to correct their folly by restoring Glass-Steagall, thus eliminating the massive bubble of gambling values and erecting a firewall between the uncontrolled speculation on Wall Street and the livelihood of the American people — precisely as Franklin Roosevelt did in 1933 when the Glass-Steagall Act was first enshrined into law. Instead, under the threats and intimidation of the largest financial institutions, Congress passed an unprecedented bailout of the Wall Street banks, on the backs of an already destitute American population. Over the subsequent eight years, our people have suffered the mounting effects of this fraud, to the point that our nation now faces another financial blowout of far-greater magnitude than even that of 2007-2008. The only means of avoiding such a fate is the immediate restoration of Glass-Steagall today as the necessary first step to a full FDR-style recovery program, as has been spelled out in detail by LaRouchePAC.

Glass-Steagall put properly, is not a federal regulation aimed at restraining the criminal temptations of an otherwise happy-go-lucky Wall Street. Glass-Steagall’s aim is to “throw the money changers out of the temple of our civilization”, once again, as President Franklin D. Roosevelt had the courage to do. It is not an adjustment within an otherwise operable system. Glass-Steagall is a revolution in national policy, a Declaration of Independence against an oppressive regime.

Glass-Steagall will not regulate Wall Street, but destroy it, and put it out of its misery, once and for all. America does not need Wall Street for its economy to grow any more than a tumor would be helpful to the growth of a man. The American Credit System, long advocated by Lyndon LaRouche, is the historical beacon with which finance the nation’s future. The cult of Wall Street—the system of finance characterized by increased rates of gambling, stealing, and fraud, has, once again, nearly destroyed the United States and therefore itself. Like a cancer, it must kill you in order for it to stay alive.What’s At Stake?Just How Bad Is It?The Triple CurveTotal DerivativesHow Did It Get This Bad?Takedown of Glass-SteagallNomi Prins on Glass-Steagall“Nobody Could Have Known”LaRouche on the Record 2008“But, Give Dodd-Frank a Chance!”The Fight For Glass-Steagall TodayContact your member of CongressNational and International SupportS.881H.R. 790

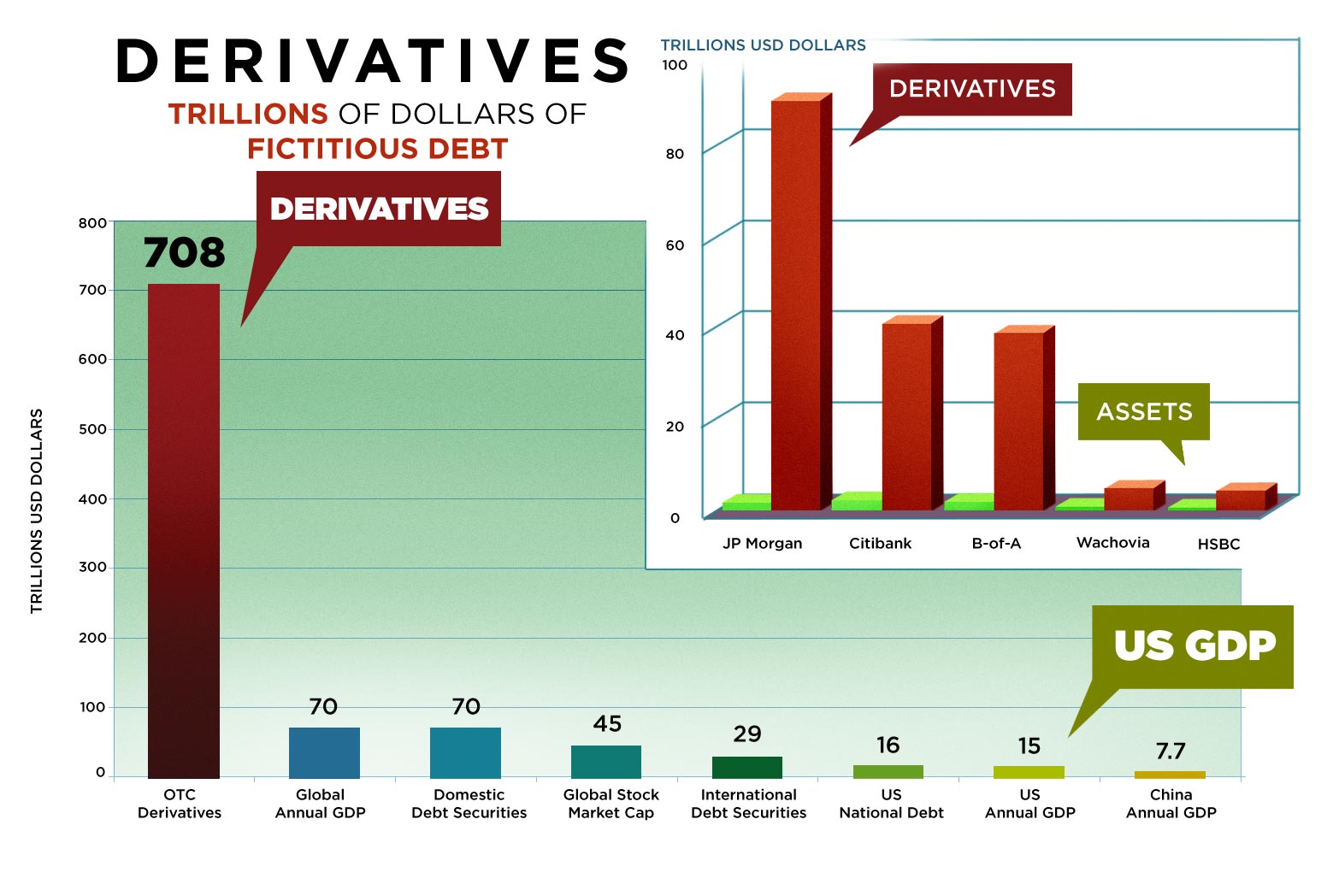

Estimates are that the current magnitude of outstanding derivatives claims accumulated as a product of speculative financial practices (read: gambling debts), now measures in the hundreds of trillions of dollars, perhaps reaching even to quadrillions. Even when compared to the current nominal global GDP, estimated at around $70 trillion, it becomes immediately apparent that this debt can never be paid. The vast majority of these outstanding claims are of a purely speculative character, with absolutely no connection to legitimate, necessary, productive economic activity. To continue to bail out this vast bubble of gambling obligations on the back of a collapsed and rapidly shrinking real economy, would be to create, rapidly, Weimar-style hyperinflation on a global scale, and an economic crisis of Dark Age proportions.

“The Triple Curve” was first presented by Mr. LaRouche at a conference at the Vatican in 1995. The version seen above is the third in a series, and functions as a heuristic device to describe the generalized collapse function of the world economy since 1971. The only way to stem the further collapse of the system is by using a Glass-Steagall standard to reorganize the transatlantic economy such that the monetary and financial aggregates of the economy conform to an increase in the physical economic input-output of the system, versus a decrease.

Glass-Steagall halts this catastrophe. By restoring the separation between commercial and investment banking, Glass-Steagall divides the obligations in question into two distinct and separate categories: legitimate and illegitimate, the latter being far greater than the former. Immediately, we declare that the government has no responsibility to pay back losses accrued through speculative activity, thus transferring these trillions in liabilities off of the government’s books. We force the megabanks—JP Morgan Chase, Citigroup, Morgan Stanley, etc.—to split themselves in two parts: the so-called “investment arms” on the one side, and plain, old-fashioned commercial banking on the other.

Under the original Glass-Steagall law, only commercial banks receive federal guarantees; “investment houses” do not enjoy such protection. Though their trillions in outstanding “assets” might not be explicitly cancelled or eliminated by law, we will simply declare that these debts are their own, their responsibility, and not the American people’s. Not one penny of bailout goes to pay them off, and, without this artificial protection, these assets will quickly dry up on their own. We as a nation are freed from this cancer, and our commercial banking system is restored to its necessary and indispensable function. This was the stated intention of Franklin Roosevelt’s original 1933 Glass-Steagall Act.

How Did It Get This Bad?

Originally produced in September 2010, LaRouchePAC’s “The Takedown of Glass-Steagall” provides the historical context for the crisis we are in today. This was LaRouchePAC’s challenge to the Democratic Party: to survive, it must cease being the party of Barack Obama and the Wall Street interests who own him. These historic oligarchic interests are what is destroying the United States today, by controlling key elected officials, such as then chairman of the House Financial Services Committee, Barney Frank, author of Obama’s infamous Wall Street reform legislation. The American people must go over the heads of Congress and the President, cut a wedge through party lines, and deliver themselves the prosperity they require.

Nomi Prins on Glass-Steagall

Nomi Prins delivers remarks to the Schiller Institute’s 30th anniversary conference, discussing her latest book “All The Presidents’ Bankers,” which details the “historical alignment of the White House and Wall Street” from Teddy Roosevelt to Barack Obama.

In 2007, during a live, international webcast, Lyndon LaRouche made a prophetic economic forecast:“There is no possibility of a non-collapse of the present financial system—none! It’s finished, now! The present financial system can not continue to exist under any circumstances, under any Presidency, under any leadership, or any leadership of nations. Only a fundamental and sudden change in the world monetary-financial system will prevent a general, immediate chain-reaction type of collapse. At what speed we don’t know, but it will go on, and it will be unstoppable!”

Then, in 2008, LaRouche was one of the first and only economists who knew that without a Glass-Steagall reorganization of the transatlantic economy, there would be no hope for a recovery.